Q1 February 2026 Sustainability Reporting one pager

Q1 February 2026 Sustainability Reporting one pagerBlog post description.

2/19/20264 min read

Veltriqa Information Summary: Key Developments in Global Sustainability Reporting – Early 2026 Outlook for Accountants

As we enter 2026, the global sustainability reporting landscape continues to evolve rapidly, with significant implications for compliance, risk management, and stakeholder transparency. This summary, prepared for accounting professionals, distills the latest updates from major frameworks including California's climate disclosure laws (SB 253 and SB 261), the EU Taxonomy, and the International Sustainability Standards Board (ISSB) IFRS Sustainability Disclosure Standards. These developments emphasize phased implementation, transitional reliefs, and simplifications to balance investor needs with practical reporting burdens.

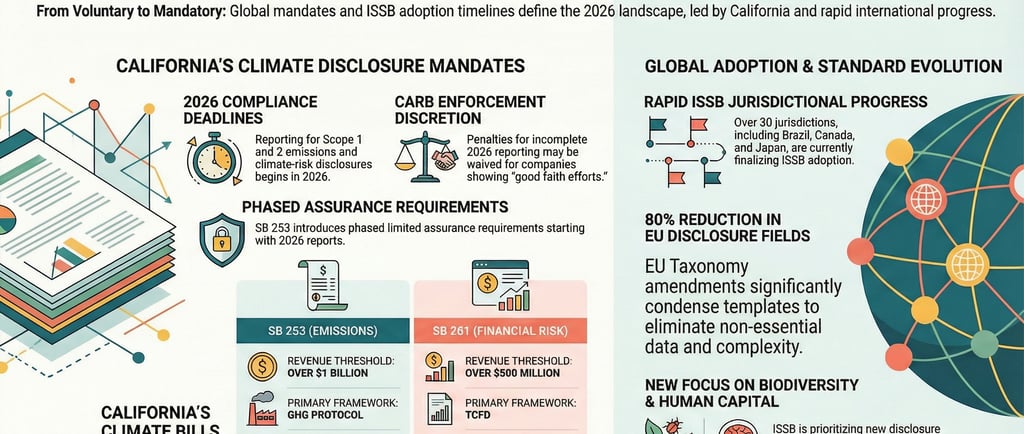

California's Climate Disclosure Laws: SB 253 and SB 261

California's landmark bills require U.S.-based entities (including subsidiaries of non-U.S. parents) "doing business in California" to disclose climate-related information. Applicability hinges on revenue thresholds (based on the lesser of the prior two fiscal years) and state nexus definitions.

Key Differences:

SB 253 (Climate Corporate Data Accountability Act) focuses on greenhouse gas (GHG) emissions reporting using the GHG Protocol. It mandates annual disclosures of Scope 1 and Scope 2 emissions starting in 2026 (proposed deadline: August 10, 2026, for prior fiscal year data), with Scope 3 commencing in 2027. Limited assurance begins in 2026 for Scope 1/2, progressing to reasonable assurance by 2030.

SB 261 (Climate-Related Financial Risk Act) requires biennial public reporting on climate-related financial risks (physical and transition) and mitigation measures, aligned with the Task Force on Climate-related Financial Disclosures (TCFD) framework or equivalents (e.g., IFRS S2). Initial statutory deadline was January 1, 2026, but enforcement is currently paused due to a Ninth Circuit injunction and CARB's advisory confirming no penalties during the stay. Voluntary reporting remains possible via a public docket.

Exemptions and Reliefs:

Statutory exemptions include government entities (and majority-owned companies), insurance-regulated entities (for SB 261), and the University of California (SB 253-specific).

Proposed additional exemptions (via draft regulations) cover non-profits/charitable organizations (IRC tax-exempt), entities with only teleworking employees in California, and those solely engaged in wholesale electricity transactions.

For initial 2026 SB 253 reporting, entities may use existing data, voluntary programs, or CARB templates. CARB's enforcement notice emphasizes "good faith efforts" with no penalties for 2026 non-compliance if demonstrated, allowing flexibility during transition.

Accountants should monitor the ongoing rulemaking (public comment closed February 2026; hearing held February 26, 2026) and litigation outcomes, as these will finalize deadlines, fees, and applicability details.

EU Taxonomy: Recent Simplifications

The European Commission adopted measures in 2025 (effective for reports from 2026 covering 2025 financial year) to reduce administrative burdens under the EU Taxonomy framework.

Key changes include:

Streamlined templates — Reduced significantly in datapoints, with new summary tables for turnover, CapEx, and OpEx KPIs. Specific templates for fossil gas and nuclear activities eliminated.

Materiality threshold — A 10% cumulative threshold applies: Non-financial entities exclude activities below 10% of turnover, CapEx, or OpEx from eligibility/alignment assessments. Financial entities gain similar reliefs, limiting reporting to exposures to CSRD-in-scope entities and allowing delayed or omitted templates in certain cases.

Simplified "Do No Significant Harm" criteria for pollution prevention (e.g., chemical use).

These updates support non-financial and financial entities in focusing on material impacts while maintaining alignment with sustainability objectives.

ISSB IFRS Sustainability Disclosure Standards: Global Adoption and Updates

The International Sustainability Standards Board (ISSB) develops the IFRS Sustainability Disclosure Standards (IFRS S1 for general sustainability-related risks/opportunities; IFRS S2 for climate-specific disclosures), providing a consistent global baseline for investor-focused reporting.

Adoption Progress: Global uptake is accelerating, with jurisdictions such as Australia, Malaysia, and Nigeria having finalized approaches, while others (e.g., Canada, China, UK) advance implementation. Many align with or incorporate IFRS S1/S2 for baseline consistency.

Recent Developments:

Targeted amendments to IFRS S2 (issued December 2025, effective January 1, 2027, early adoption permitted) address GHG challenges:

Relief for Scope 3 Category 15 (financed emissions): Entities may limit disclosures to financed emissions only.

Jurisdictional relief: Flexibility where local requirements mandate different measurement methods (beyond strict GHG Protocol 2004).

Clarifications on classification and global warming potentials.

SASB Standards enhancements — Ongoing amendments across 41 industries (prioritizing extractives, processed foods, and others) to align with IFRS S2 industry-based guidance, focusing on climate topics like water management.

Future priorities — Research and projects on Biodiversity, Ecosystems, and Ecosystem Services (BEES), plus Human Capital, to expand beyond climate.

These standards integrate with frameworks like TCFD (now retired) and support interoperability with regional rules (e.g., California disclosures).

Implications for Accountants

Accountants play a pivotal role in assessing scope, ensuring data quality, applying transitional reliefs, and preparing for assurance requirements. Key focus areas include:

Evaluating entity applicability via revenue and jurisdictional tests.

Documenting good faith efforts and retaining records.

Aligning disclosures across frameworks (e.g., GHG Protocol, TCFD/IFRS S2).

Monitoring 2026–2027 transitions, including Scope 3 phasing and amendments.

Veltriqa remains committed to supporting clients with tailored compliance strategies amid these dynamic requirements. For personalized assessments or further details on implementation, contact our team.

This summary is based on publicly available regulatory updates as of early 2026 and does not constitute legal advice. Always consult official sources and professional guidance for specific applications.

Resources Used The information in this summary is derived from publicly available official and authoritative sources to ensure accuracy and compliance with copyright principles (no proprietary content reproduced verbatim; summaries and syntheses only):

California Air Resources Board (CARB) official website: Primary program page and regulatory materials for SB 253 and SB 261 – https://ww2.arb.ca.gov/our-work/programs/california-corporate-greenhouse-gas-ghg-reporting-and-climate-related-financial

CARB Enforcement Advisory (December 1, 2025) and related notices – Available via CARB's climate disclosure resources

European Commission – Finance Directorate-General: EU Taxonomy simplification measures and Delegated Act details – https://finance.ec.europa.eu/regulation-and-supervision/financial-services-legislation/implementing-and-delegated-acts/taxonomy-regulation_en

International Sustainability Standards Board (ISSB) / IFRS Foundation: Announcements on IFRS S2 amendments (December 2025) and SASB enhancements – https://www.ifrs.org/news-and-events/news/2025/12/issb-issues-targeted-amendments-ifrs-s2

IFRS Foundation project pages on enhancing SASB Standards – https://www.ifrs.org/projects/work-plan/enhancing-the-sasb-standards/ed-cl-sasb

These sources provide the foundational regulatory texts, announcements, and guidance upon which this professional overview is based.